EU Taxonomy Overview

By passing the Green Deal in 2019, the European Union (EU) set the course for more sustainable investments, for example in areas like renewable energy, biodiversity or circular economy. The goal is to reach a climate-neutral economy in the EU by 2050, with a reduction of 55% already implemented in 2030. To achieve these climate goals, the Green Deal includes an investment plan of 1 trillion euros over the next 10 years. Despite this huge investment, the EU depends also on the support of the private sector to achieve the Paris climate agreement.

The EU Taxonomy regulation and the Sustainable Finance Disclosure Regulation (SFDR) are implemented to ensure equal competition and legal certainty for all companies operating within the EU. Both regulations follow the objective of the Green Deal and have the following key goals:

Reorientation of capital flows with a focus on sustainable investments

Establishing sustainability as a component of risk management

Promoting/encouraging long-term investment and economic activity

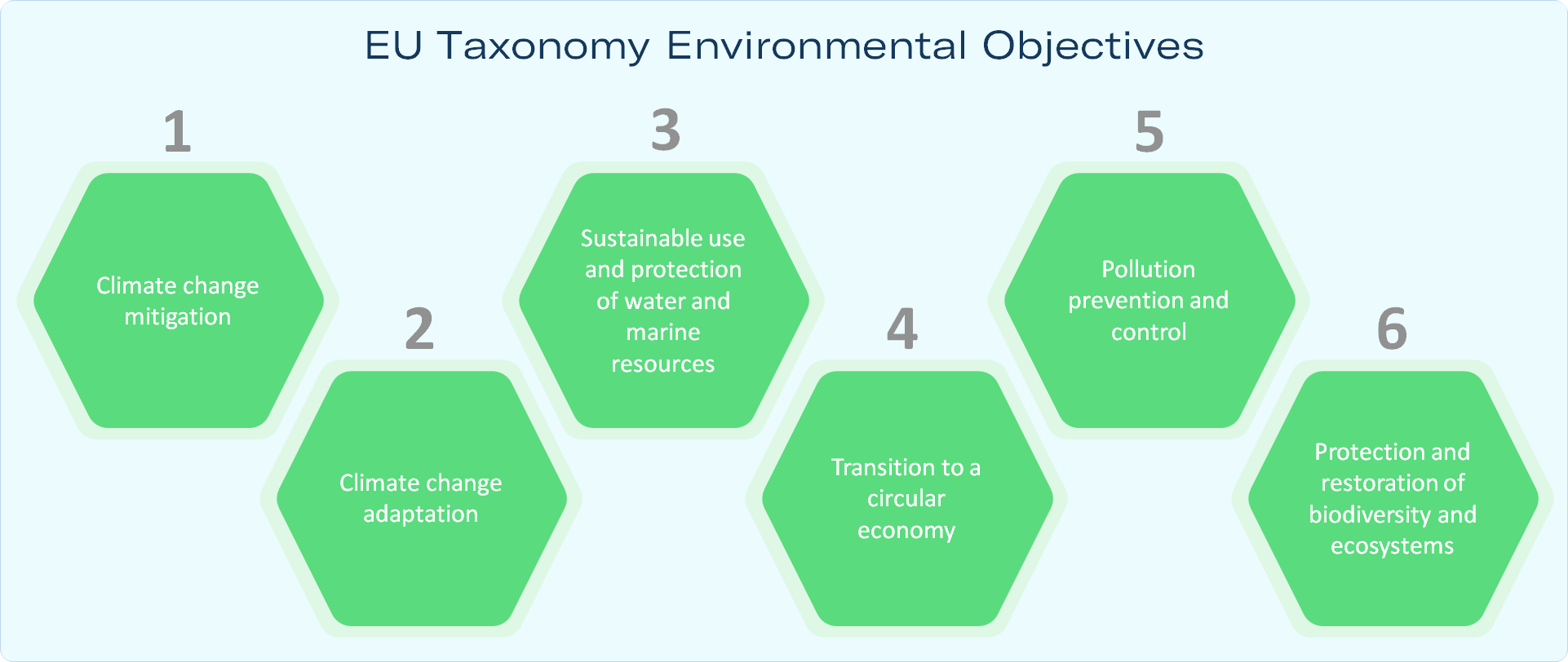

The EU taxonomy regulation describes a framework to classify “green” or “sustainable” economic activities executed in the EU. Previously, there was no clear definition of green, sustainable or environmentally friendly economic activity. The EU taxonomy regulation creates a clear framework for the concept of sustainability, exactly defining when a company or enterprise is operating sustainably or environmentally friendly. Compared to their competitors, these companies stand out positively and thus should benefit from higher investments. Thereby, the legislation aims to reward and promote environmentally friendly business practices and technologies. The focus lays on the following six environmental objectives:

Climate change mitigation

Climate change adaptation

Sustainable use and protection of water and marine resources

Transition to a circular economy

Pollution prevention and control

Protection and restoration of biodiversity and ecosystems

To be classified as a sustainable economic activity according to the EU taxonomy regulation, a company must not only contribute to at least one environmental objective but also must not violate the remaining ones. An activity aiming to mitigate the climate but at the same time also negatively affecting biodiversity cannot be classified as sustainable. The classification of an economic activity in terms of sustainability is based on the following four criteria, which base on the previously mentioned environmental objectives:

The economic activity contributes to one of the six environmental objectives

The economic activity does ‘no significant harm’ (DNSH) to any of the six environmental objectives

The economic activity meets ‘minimum safeguards’ such as the UN Guiding Principles on Business and Human Rights to not have a negative social impact

The economic activity complies with the technical screening criteria developed by the EU Technical Expert Group

The fourth criterion of the EU taxonomy refers to technical solutions for emission reduction and is so far based on a draft by the Technical Expert Group from 2020. In April 2021, the first details for the two environmental objectives of climate change mitigation and adaptation were released. Detailed information for the four remaining environmental objectives is expected in the course of this year (2021). Those details are expected to be adjusted regularly to reflect the current technological state of the art.

Our software helps evaluating and documenting your activities, as well as with the calculation of the key figures

Just send us a message. We will come back to you as fast as possible according to your request.